CALGARY, ALBERTA–(Marketwired – March 13, 2017) – Cardinal Energy Ltd. (“Cardinal” or the “Company“) (TSX:CJ) is pleased to announce its operating and financial results for the quarter and year ended December 31, 2016 as well as its 2016 year end reserves.

| FINANCIAL AND OPERATING HIGHLIGHTS | ||||||||||||||

| ($ 000’s except shares, per share and operating amounts) | Three months ended December 31 | Year ended December 31 | ||||||||||||

| 2016 | 2015 | % Change | 2016 | 2015 | % Change | |||||||||

| Financial | ||||||||||||||

| Petroleum and natural gas revenue | 58,721 | 43,300 | 36 | 195,942 | 178,100 | 10 | ||||||||

| Cash flow from operating activities | 9,728 | 9,121 | 7 | 60,962 | 86,735 | (30 | ) | |||||||

| Adjusted funds flow(1) | 16,247 | 17,955 | (10 | ) | 59,104 | 94,646 | (38 | ) | ||||||

| basic and diluted per share | $ | 0.22 | $ | 0.29 | (23 | ) | $ | 0.84 | $ | 1.61 | (48 | ) | ||

| Dividends declared | 7,747 | 13,664 | (43 | ) | 29,584 | 49,911 | (41 | ) | ||||||

| per share | $ | 0.105 | $ | 0.21 | (50 | ) | $ | 0.42 | $ | 0.84 | (50 | ) | ||

| Net bank debt (1) | 70,300 | 96,185 | (27 | ) | 70,300 | 96,185 | (27 | ) | ||||||

| Exploration and development capital | 14,510 | 11,055 | 31 | 41,361 | 36,571 | 13 | ||||||||

| Acquisitions, net | 33,229 | 130,822 | (75 | ) | 34,235 | 162,364 | (79 | ) | ||||||

| Total capital expenditures | 47,927 | 142,066 | (66 | ) | 76,258 | 199,703 | (62 | ) | ||||||

| Weighted average shares outstanding | ||||||||||||||

| basic and diluted (000s) | 73,728 | 62,957 | 17 | 70,097 | 58,852 | 19 | ||||||||

| Operating | ||||||||||||||

| Average daily production | ||||||||||||||

| Crude oil and NGL (bbl/d) | 12,586 | 12,176 | 3 | 12,771 | 10,792 | 18 | ||||||||

| Natural gas (mcf/d) | 12,178 | 9,696 | 26 | 11,042 | 6,273 | 76 | ||||||||

| Total (boe/d) | 14,616 | 13,792 | 6 | 14,611 | 11,838 | 23 | ||||||||

| Netback(1) | ||||||||||||||

| Petroleum and natural gas revenue | $ | 43.67 | $ | 34.13 | 28 | $ | 36.64 | $ | 41.22 | (11 | ) | |||

| Royalties | 5.57 | 4.20 | 33 | 4.61 | 5.19 | (11 | ) | |||||||

| Operating expenses | 23.24 | 23.66 | (2 | ) | 21.23 | 22.43 | (5 | ) | ||||||

| Netback | $ | 14.86 | $ | 6.27 | 137 | $ | 10.80 | $ | 13.60 | (21 | ) | |||

| Realized hedging gain | $ | 0.09 | $ | 11.02 | (99 | ) | $ | 3.08 | $ | 11.59 | (73 | ) | ||

| Netback after risk management | $ | 14.95 | $ | 17.29 | (14 | ) | $ | 13.88 | $ | 25.19 | (45 | ) | ||

| (1) See non-GAAP measures | ||||||||||||||

2016 Financial and Operating Highlights

- Average production for the year ended December 31, 2016 increased 23% to 14,611 boe/d from 11,838 boe/d in 2015, with a 2016 exit rate of approximately 15,000 boe/d.

- Cardinal’s average annual production per debt adjusted share increased by 6% to 189 boe/d per million debt adjusted shares in 2016 from 178 boe/d per million debt adjusted shares in 2015.

- Operating costs per boe for the year decreased by 5% to $21.23/boe in 2016 from $22.43/boe in 2015.

- General and administrative expenses per boe for the year ended December 31, 2016 decreased by 21% to $1.98/boe from $2.51/boe in 2015.

- Bank debt at December 31, 2016 decreased to $61.3 million, from $91.8 million at December 31, 2015.

Cardinal achieved exit fourth quarter 2016 record production of just over 15,000 boe/d. Q4 production was 23% higher in 2016 versus 2015 despite lost production time due to TCPL shutdowns and delays in new drill additions due to scheduled fracs being delayed by frac providers.

Cardinal’s fourth quarter capital program included 3 wells which were drilled in Q4 2016 but are not expected to contribute to production and adjusted funds flow until Q1 and Q2 2017. Adjusted for these wells, Cardinal’s total payout ratio was less than 100%.

2016 was a transitional year for Cardinal as we recovered from low commodity prices. We are set to benefit from the rebound in commodity prices with increased spending for 2017. Cardinal will drill a record number of wells this year targeting multiple plays across our asset base. We have aggressively started 2017 with the drilling of 3 (1.9 net) successful full length horizontal wells at Mitsue and 5 horizontal wells at Bantry. This has been Cardinal’s most active Q1 drilling program since the Company’s inception and we look forward to reporting drill results in the future.

Acquisitions are a core part of Cardinal’s business strategy and although 2016 was a quiet year on the M&A front, we closed an acquisition in Wainwright in late Q4 for $32 million. The acquisition added low decline medium oil production to our production base. We expect to achieve operational synergies on the acquisition throughout 2017 as we are able to shut in an oil battery offsetting the acquired lands and process our oil at the newly acquired facility.

Cardinal’s balance sheet remains strong and allows us to execute an active capital program and selectively acquire assets. After accounting for the Wainwright acquisition, Cardinal ended 2016 with $70 million in net bank debt less our convertible debentures outstanding, approximately $26 million lower than at year end 2105. Our bank credit facility is set at $150 million.

Cardinal pays a monthly dividend which is an important component of our business strategy and how we deliver value to our shareholders. We believe that we have created a sustainable business model that is able to fund its dividend through payment in cash. By suspending our dividend Reinvestment Plan (“DRIP”) and our Stock Dividend Program (“SDP”) we will be able to further maximize shareholder value by eliminating the dilution that the DRIP and SDP had on our per share performance. Eliminations of both programs will apply to our May 15, 2017 dividend payment to shareholder of record on April 28, 2017. Shareholders that were in the program will now automatically receive their dividend payment in cash.

Cardinal’s 2016 year end reserves evaluation confirms the low risk characteristics of our assets. Despite a quiet year operationally, (only 9 wells were drilled in Bantry) we managed to replace our production by 250% on a proved plus probable (“2P”) basis. Our total proved (“1P”) and 2P reserves increased on a per share basis again in 2016. Proved plus probable producing reserves make up 86% of our reserves.

Despite a 14% decrease in forecast reserve prices from 2015 to 2016, the value of Cardinal’s 2P reserves increased slightly on NPV10, before tax basis to $860 million.

Cardinal increased its undeveloped reserves this year by adding an additional ten 2P undeveloped locations to its reserves booking. Future Development Capital (“FDC”) increased to $64.9 million in 2016 which is designed to be approximately 1 year spending capabilities (adjusted funds flow less dividends).

Cardinal added 10.6 Mmboe of reserves in 2016 through drilling and positive technical reserve additions.

Cardinal’s net asset value as at December 31, 2016 is summarized below:

| NAV | $/share |

| PDP | $9.60 |

| PNP+PUD | $0.50 |

| Probable | $2.29 |

| TPP Reserves | $12.38 |

| ARO | -$0.79 |

| Land | $0.08 |

| Debt | -$0.95 |

| TOTAL NAV/Share (basic) | $10.73 |

2016 Reserve Highlights

- Total 2P reserves increased by 13% to 67 Mmboe in 2016. On a debt adjusted per share basis, 2P reserves increased by 7% (basic) and 6% (fully diluted excluding debentures) from 2015.

- Increased total 1P reserves by 12% to 49 Mmboe in 2016. 1P reserves on a debt adjusted per share basis increased 6% (basic) and 5% (fully diluted excluding debentures) from 2015. Proved reserves make up 73% of Cardinal’s 2P reserves.

- Cardinal achieved a recycle ratio of 1.9 including realized gains on commodity contracts on a proved plus probable basis.

- Cardinal’s proved producing reserve life index (“RLI”) increased by 4% to 8.5 years, its proved reserve life index increased by 7% to 9.3 years and its 2P reserve life index increased 8% to 12.7 years based on fourth quarter average production of 14,616 boe/d.

- In 2016, Cardinal’s 2P reserve additions replaced 250 percent of its annual production, primarily with proved producing reserves.

- Net present value (“NPV”) before tax discounted at 10% (“NPV10”) of 2P reserves was $860 million. Cardinal currently has approximately $1.1 billion of tax pools.

- 2016 finding and development costs including the change in FDC were $5.59 on a 1P basis and $5.80 on 2P basis. Three year average finding and development costs including the change in FDC were $9.38 on a 1P basis and $10.09 on a 2P basis.

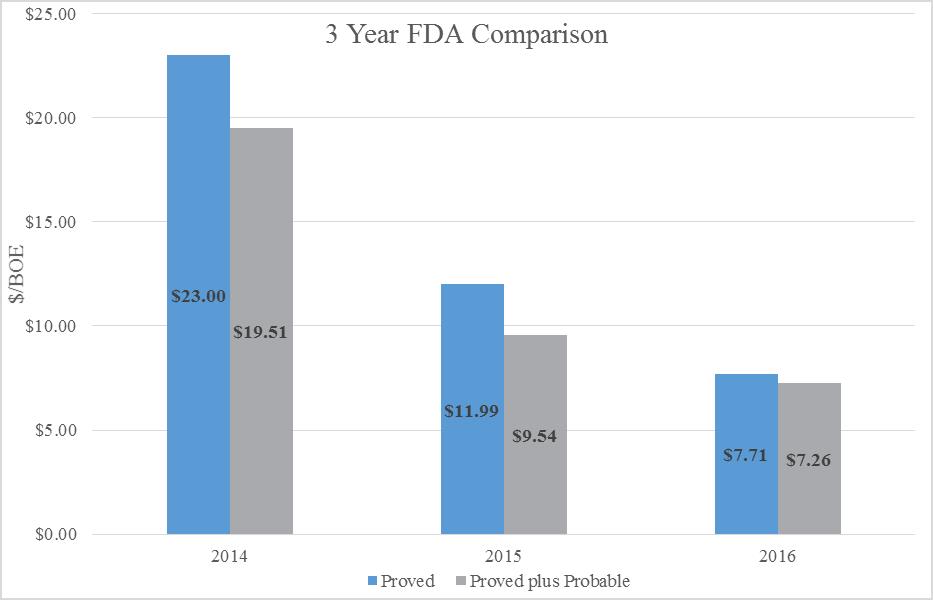

- Finding, development and acquisition costs including the change in FDC in 2016 were $7.71 per boe on a 1P basis and $7.26 on a 2P basis. Three year average finding, development and acquisition costs including the change in FDC were $15.87 on a 1P basis and $13.22 on a 2P basis.

To view the 3 Year FDA Comparison, please click this link: http://media3.marketwire.com/docs/8695c.jpg

{kind=link}

Summary of Reserves

Cardinal’s year end 2016 reserves were evaluated by independent reserves evaluators Sproule Associates Ltd. (“Sproule”) and GLJ Petroleum Consultants (“GLJ”). These evaluations of all of the Company’s oil and gas properties were done in accordance with the definitions, standards and procedures contained in the Canadian Oil and Gas Evaluation Handbook (“COGE Handbook”) and National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in Cardinal’s Annual Information Form which will be filed on SEDAR on or before March 30, 2017.

Summary of Oil and Gas Reserves(3)

| Yearend 2016(1)(5) | Yearend 2015(2)(6) | |

| At December 31 | Equivalents (mboe) | Equivalents (mboe) |

| Proved producing | 45,416 | 41,469 |

| Proved non-producing | 2,220 | 1,164 |

| Proved undeveloped | 1,816 | 1,357 |

| Total proved | 49,452 | 43,990 |

| Probable additional | 18,024 | 15,535 |

| Total proved and probable | 67,476 | 59,525 |

| Proved producing RLI, (yrs)(5)(6) | 8.5 | 8.2 |

| Proved RLI, (yrs) (5)(6) | 9.3 | 8.7 |

| Proved and probable RLI, (yrs) (5)(6) | 12.7 | 11.8 |

| Proved plus probable producing RLI, (yrs) (5)(6) | 10.9 | 10.8 |

| Proved and Probable producing reserves % of Total | 86% | 92% |

| NPV10 Before Income Tax 10%(1) |

NPV10 Before Income Tax 10%(2) |

|

| At December 31 | (M$) | (M$) |

| Proved producing | 653,138 | 668,665 |

| Proved non-producing | 22,029 | 12,404 |

| Proved undeveloped | 15,108 | 11,098 |

| Total Proved | 690,275 | 692,167 |

| Probable additional | 169,493 | 165,138 |

| Total Proved and Probable | 859,768 | 857,305 |

| (1) Based on Sproule’s December 31, 2016 price forecast. |

| (2) Based on Sproule’s December 31, 2015 price forecast. |

| (3) Gross reserves are the Company’s total working interest reserves before deduction of royalties and without including royalty interest reserves. |

| (4) Numbers may not add due to rounding. |

| (5) RLI based on 14,600 boed as at December 31, 2016. |

| (6) RLI based on 13,800 boed as at December 31, 2015. |

Reserves Reconciliation

| Gross Reserves | ||||||

| PDP | Proved | Proved and Probable |

||||

| December 31, 2015 | 41,469 | 43,990 | 59,525 | |||

| Extensions & Improved Recovery | 1,464 | 1,983 | 3,334 | |||

| Technical Revisions(3) | 5,793 | 6,738 | 7,306 | |||

| Acquisitions (1) | 2,030 | 2,081 | 2,650 | |||

| Production | (5,340 | ) | (5,340 | ) | (5,340 | ) |

| December 31, 2016 | 45,416 | 49,452 | 67,476 | |||

| 2016 Reserve Additions(2) | 9,288 | 10,802 | 13,291 | |||

| Production Replacement x | 1.7 | 2.0 | 2.5 | |||

| (1) In accordance with the requirements of NI 51-101, the reserve estimates for acquisitions are the reserves as of December 31, 2016 plus production from date of acquisition date. |

| (2) 86% of the 1P reserve additions are proved producing reserves. |

| (3) Includes any revisions for economic factors. |

LMR Update

Cardinal’s Liability Management Rating (“LMR”) continues to be reduced on a monthly basis. We expect that our LMR will exceed 2 in the second quarter of 2017 and that we will be able to maintain a continually improving ratio above 2 on a go forward basis.

Outlook

Cardinal intends to continue to maintain a prudent approach to capital management while focusing on balance sheet strength and maintaining a significant and sustainable dividend all within adjusted funds flow. Cardinal remains constructive on a crude oil price recovery through-out 2017 and has started executing a budget that focuses on development of all three of our core areas and expects an average annual production increase between 15% and 18% over 2016. We expect this approach to deliver strong returns to shareholders in 2017 and beyond.

The low decline nature of our base production requires a limited number of wells each year to replace production. Our 2017 capital program is broader than in previous years and has drilling in all three of our core areas. The major components of the 2017 capital budget are $16 million for facilities and pipelines, $32.7 million for the drilling of 18 wells as well as to spend $4 million on environmental and reclamation initiatives. We will continue to evaluate acquisition opportunities through the year with the goal of increasing our light oil weighting and drilling inventory.

Cardinal maintains a conservative borrowing policy. At year end we had approximately $70 million drawn on our $150 million credit facility. Our borrowing base is currently set by our lenders at $250 million and Cardinal chooses to maintain a smaller credit facility.

Annual Filings

Cardinal also announces the filing of its Audited Financial Statements for the year ended December 31, 2016 and related Management’s Discussion and Analysis with the Canadian securities regulatory authorities on the System for Electronic Analysis and Retrieval (“SEDAR”). In addition, Cardinal expects to file its Annual Information Form for the year ended December 31, 2016 on SEDAR on or prior to March 30, 2017. Electronic copies may be obtained on Cardinal’s website at www.cardinalenergy.ca and on Cardinal’s SEDAR profile at www.sedar.com.

March Dividend

Cardinal confirms that a dividend of $0.035 per common share will be paid on April 18, 2017 to shareholders of record on March 31, 2017. The Board of Directors of Cardinal has declared the dividend payable in the form either cash or common shares at the election of the shareholder. This dividend has been designated as an “eligible dividend” for Canadian income tax purposes.

About Cardinal Energy Ltd.

Cardinal is a junior Canadian oil focused company built to provide investors with a stable platform for dividend income and growth. Cardinal’s operations are focused in all season access areas in Alberta.

Note Regarding Forward-Looking Statements

This press release contains forward-looking statements and forward-looking information (collectively “forward-looking information”) within the meaning of applicable securities laws relating to the Cardinal’s plans and other aspects of Cardinal’s anticipated future operations, management focus, objectives, strategies, financial, operating and production results. Forward-looking information typically uses words such as “anticipate”, “believe”, “project”, “expect”, “goal”, “plan”, “intend”, ” may”, “would”, “could” or “will” or similar words suggesting future outcomes, events or performance. The forward-looking statements contained in this press release speak only as of the date thereof and are expressly qualified by this cautionary statement.

Specifically, this press release contains forward-looking statements relating to: our business strategies, plans and objectives, future production and production decline rates, acquisition plans, dividend policy and plans, planned capital expenditures and the allocation thereof, and the anticipated results therefrom, the timing and results of the semi-annual review of our credit facility, future commodity prices, expected operational synergies on the Wainwright acquisition, timing of the suspension of the DRIP and SDP and the benefits to be obtained as a result of the suspension and estimated tax pools. In addition, information and statements relating to reserves are deemed to be forward-looking statements, as they involve implied assessment, based on certain estimates and assumptions, that the reserves described exist in quantities predicted or estimated, and that the reserves can be profitably produced in the future.

Forward-looking statements regarding Cardinal are based on certain key expectations and assumptions of Cardinal concerning anticipated financial performance, business prospects, strategies, regulatory developments, current commodity prices and exchange rates, applicable royalty rates, tax laws, future well production rates and reserve volumes, future operating costs, the performance of existing and future wells, the success of its exploration and development activities, the sufficiency and timing of budgeted capital expenditures in carrying out planned activities, the availability and cost of labor and services, the impact of competition, conditions in general economic and financial markets, availability of drilling and related equipment, effects of regulation by governmental agencies, the ability to obtain financing on acceptable terms which are subject to change based on commodity prices, market conditions, drilling success and potential timing delays.

These forward-looking statements are subject to numerous risks and uncertainties, certain of which are beyond Cardinal’s control. Such risks and uncertainties include, without limitation: the impact of general economic conditions; volatility in market prices for crude oil and natural gas; industry conditions; currency fluctuations; imprecision of reserve estimates; liabilities inherent in crude oil and natural gas operations; environmental risks; incorrect assessments of the value of acquisitions and exploration and development programs; competition from other producers; the lack of availability of qualified personnel, drilling rigs or other services; changes in income tax laws or changes in royalty rates and incentive programs relating to the oil and gas industry; hazards such as fire, explosion, blowouts, and spills, each of which could result in substantial damage to wells, production facilities, other property and the environment or in personal injury; and ability to access sufficient capital from internal and external sources.

Management has included the forward-looking statements above and a summary of assumptions and risks related to forward-looking statements provided in this press release in order to provide readers with a more complete perspective on Cardinal’s future operations and such information may not be appropriate for other purposes. Cardinal’s actual results, performance or achievement could differ materially from those expressed in, or implied by, these forward-looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits that Cardinal will derive there from. Readers are cautioned that the foregoing lists of factors are not exhaustive. These forward-looking statements are made as of the date of this press release and Cardinal disclaims any intent or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or results or otherwise, other than as required by applicable securities laws.

Non-GAAP measures

This press release contains the terms “adjusted funds flow”, “total payout ratio”, “net debt”, “net bank debt”, “development capital expenditures”, “netback”, “netback after risk management” which do not have a standardized meaning prescribed by International Financial Reporting Standards (“IFRS” or, alternatively, “GAAP”) and therefore may not be comparable with the calculation of similar measures by other companies. Cardinal uses adjusted funds flow and total payout ratio to analyze operating performance and assess leverage. Cardinal feels these benchmarks are key measures of profitability and overall sustainability for the Company. Adjusted funds flow and total payout ratio are not intended to represent operating profits nor should they be viewed as an alternative to cash flow provided by operating activities, net earnings or other measures of performance calculated in accordance with GAAP. Adjusted funds flow is calculated as cash flows from operating activities adjusted for changes in non-cash working capital and decommissioning expenditures. Total payout ratio represents the ratio of the sum of dividends declared plus development capital expenditures divided by adjusted funds flow. Total payout ratio is another key measure to assess our ability to finance operating activities, capital expenditures and dividends. Net bank debt is calculated as bank debt plus the principal amount of convertible unsecured subordinated debentures and current liabilities less current assets (adjusted for the fair value of financial instruments and the current portion of the decommissioning obligation). Net bank debt is used by management to analyze the financial position, liquidity and leverage of Cardinal. Development capital expenditures represent expenditures on property, plant and equipment (excluding corporate and other assets and acquisitions) to maintain and grow the Company’s base production. Netback is calculated on a boe basis and is determined by deducting royalties and operating expenses from petroleum and natural gas revenue. Netback is utilized by Cardinal to better analyze the operating performance of its petroleum and natural gas assets against prior periods. Netback after risk management includes realized gains or losses in the period on a boe basis.

Oil and Gas Metrics

The term “boe” or barrels of oil equivalent may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet of natural gas to one barrel of oil equivalent (6 Mcf: 1 bbl) is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Additionally, given that the value ratio based on the current price of crude oil, as compared to natural gas, is significantly different from the energy equivalency of 6:1; utilizing a conversion ratio of 6:1 may be misleading as an indication of value.

This press release contains a number of additional oil and gas metrics, including finding and development costs, finding, development and acquisition costs, reserve life index and recycle ratio, which do not have standardized meanings or standard methods of calculation and therefore such measures may not be comparable to similar measures used by other companies. Such metrics have been calculated by management and included herein to provide readers with additional measures to evaluate Cardinal’s performance; however, such measures are not reliable indicators of the future performance of Cardinal and future performance may not compare to the performance in previous periods.

Finding and developments costs and finding, development and acquisition costs are used as a measure of capital efficiency. Finding and development costs are calculated on a per boe basis by dividing the aggregate of the change in future development costs from the prior year for the particular reserve category and the costs incurred on development and exploration activities in the year by the change in reserves from the prior year for the reserve category. Development and exploration expenditures include costs of land and seismic, but exclude capitalized general and administration costs. The aggregate of the exploration and development costs incurred in the most recent financial year and the change during that year in estimated future development costs generally will not reflect total finding and development costs related to reserves additions for that year. Finding development and acquisition costs are calculated on a per boe basis by dividing the aggregate of the change in future development costs from the prior year for the particular reserve category and the costs incurred on development and exploration activities and property acquisitions (net of dispositions) in the year by the change in reserves from the year for the reserve category. Acquisition costs include the announced purchase price of acquisitions rather than the amounts allocated to property, plant and equipment and exploration and evaluation assets for accounting purposes. Recycle ratio was calculated by dividing operating netback per boe (with and without realized gains on commodity contracts on a boe basis) by the finding, development and acquisition costs for the relevant reserve category for the year. Reserve life index is calculated based on the amount for the relevant reserve category divided by fourth quarter average daily production. Reserves per debt adjusted share adjusts net debt by converting net debt to equity using the closing share price of Cardinal on the Toronto Stock Exchange (“TSX”) at the year end and is calculated as year end reserves divided by the sum of the number of common shares issued and outstanding at year end and net debt at year end divided by Cardinal’s closing share price for the years. Production per debt adjusted share adjusts for net debt by converting net debt to equity using the average share price of Cardinal on the TSX for the year and is calculated as average annual production divided by the sum of the number of common shares issued and outstanding at year end and net debt at year end divided by Cardinal’s average share price for the years.

Other Oil and Gas Advisories

Unless otherwise indicated, all reserves reported in this press release are “gross reserves” which represent Cardinal’s total working interest reserves prior to the deduction of royalties payable or royalty interests paid to the Company.

Future net revenue is a forecast of revenue, estimated using forecast prices and costs arising from the anticipated development and production of resources, net of associated royalties, operating costs, development costs and abandonment and reclamation costs. It should not be assumed that the future net revenues undiscounted and discounted at 10% included in this press release represent the fair market value of the reserves.

The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties due to the effects of aggregation.

CEO

Cardinal Energy Ltd.

(403) 234-8681

Laurence Broos

VP Finance

Cardinal Energy Ltd.

(403) 234-8681

www.cardinalenergy.ca